Some common loss functions¶

There are several commonly used smooth loss functions built into

regreg:

squared error loss (

regreg.api.squared_error)Logistic loss (

regreg.glm.glm.logistic)Poisson loss (

regreg.glm.glm.poisson)Cox proportional hazards (

regreg.glm.glm.coxph, depends onstatsmodels)Huber loss (

regreg.glm.glm.huber)Huberized SVM (

regreg.smooth.losses.huberized_svm)

import numpy as np

import regreg.api as rr

import matplotlib.pyplot as plt

import rpy2.robjects as rpy2

from rpy2.robjects import numpy2ri

numpy2ri.activate()

X = np.random.standard_normal((100, 5))

X *= np.linspace(1, 3, 5)[None, :]

Y = np.random.binomial(1, 0.5, (100,))

loss = rr.glm.logistic(X, Y)

loss

rpy2.r.assign('X', X)

rpy2.r.assign('Y', Y)

r_soln = rpy2.r('glm(Y ~ X, family=binomial)$coef')

loss.solve()

np.array(r_soln)

The losses can very easily be combined with a penalty.

penalty = rr.l1norm(5, lagrange=2)

problem = rr.simple_problem(loss, penalty)

problem.solve(tol=1.e-12)

rpy2.r('''

library(glmnet)

Y = as.numeric(Y)

G = glmnet(X, Y, intercept=FALSE, standardize=FALSE, family='binomial')

print(coef(G, s=2 / nrow(X), x=X, y=Y, exact=TRUE))

''')

Suppose we want to match glmnet exactly without having to specify

intercept=FALSE and standardize=FALSE. The normalize

transformation can be used here.

n = X.shape[0]

X_intercept = np.hstack([np.ones((X.shape[0], 1)), X])

X_normalized = rr.normalize(X_intercept, intercept_column=0, scale=False)

loss_normalized = rr.glm.logistic(X_normalized, Y)

penalty_normalized = rr.weighted_l1norm([0] + [1]*5, lagrange=2.)

problem_normalized = rr.simple_problem(loss_normalized, penalty_normalized)

coefR = problem_normalized.solve(tol=1.e-12, min_its=200)

coefR

coefG = np.array(rpy2.r('as.numeric(coef(G, s=2 / nrow(X), exact=TRUE, x=X, y=Y))'))

problem_normalized.objective(coefG), problem_normalized.objective(coefR)

In theory, using the standardize=TRUE option in glmnet should be

the same as using scale=True, value=np.sqrt((n-1)/n) in

normalize, though the results don’t match without some adjustment.

This is because glmnet returns coefficients that are on the scale of

the original \(X\).

Dividing regreg’s coefficients by the col_stds corrects this.

X_intercept = np.hstack([np.ones((X.shape[0], 1)), X])

X_normalized = rr.normalize(X_intercept, intercept_column=0,

value=np.sqrt((n-1.)/n))

loss_normalized = rr.glm.logistic(X_normalized, Y)

penalty_normalized = rr.weighted_l1norm([0] + [1]*5, lagrange=2.)

problem_normalized = rr.simple_problem(loss_normalized, penalty_normalized)

coefR = problem_normalized.solve(min_its=300)

coefR / X_normalized.col_stds

rpy2.r('''

Y = as.numeric(Y)

G = glmnet(X, Y, standardize=TRUE, intercept=TRUE, family='binomial')

coefG = as.numeric(coef(G, s=2 / nrow(X), exact=TRUE, x=X, y=Y))

''')

coefG = np.array(rpy2.r('coefG'))

coefG = coefG * X_normalized.col_stds

problem_normalized.objective(coefG), problem_normalized.objective(coefR)

(67.64597880430388, 67.639665071862495)

Defining a new smooth function¶

A smooth function only really needs a smooth_objective method in

order to be used in regreg.

For example, suppose we want to define the loss

as a smooth approximation to the function

\(K=\left\{\mu: a_i^T\mu\leq b_i, 1 \leq i \leq k\right\}\) (i.e. 0 inside \(K\) and \(\infty\) outside \(K\)).

class barrier(rr.smooth_atom):

# the argumenets [coef, offset, quadratic, initial]

# are passed when a function is composed with a linear_transform

objective_template = r"""\ell^{\text{barrier}}\left(%(var)s\right)\

"""

def __init__(self,

shape,

A,

b,

coef=1.,

offset=None,

quadratic=None,

initial=None):

rr.smooth_atom.__init__(self,

shape,

coef=coef,

offset=offset,

quadratic=quadratic,

initial=initial)

self.A = A

self.b = b

def smooth_objective(self, mean_param, mode='both', check_feasibility=False):

mean_param = self.apply_offset(mean_param)

slack = self.b - self.A.dot(mean_param)

if mode == 'both':

f = self.scale(np.sum(mean_param**2/2.) - np.log(slack).sum())

g = self.scale(mean_param + self.A.T.dot(1. / slack))

return f, g

elif mode == 'grad':

g = self.scale(mean_param + self.A.T.dot(1. / slack))

return g

elif mode == 'func':

f = self.scale(np.sum(mean_param**2/2.) - np.log(slack).sum())

return f

else:

return ValueError('mode incorrectly specified')

A = np.array([[1, 0.], [1, 1]])

b = np.array([3., 4])

barrier_loss = barrier((2,), A, b)

barrier_loss

barrier_loss.solve(min_its=100)

The loss can now be combined with a penalty or constraint very easily.

l1_bound = rr.l1norm(2, bound=0.5)

problem = rr.simple_problem(barrier_loss, l1_bound)

problem.solve()

The loss can also be composed with a linear transform:

X = np.random.standard_normal((2,1))

lossX = rr.affine_smooth(barrier_loss, X)

lossX

lossX.solve()

Huberized lasso¶

The Huberized lasso minimizes the following objective

where \(H_{\delta}(\cdot)\) is a function applied element-wise,

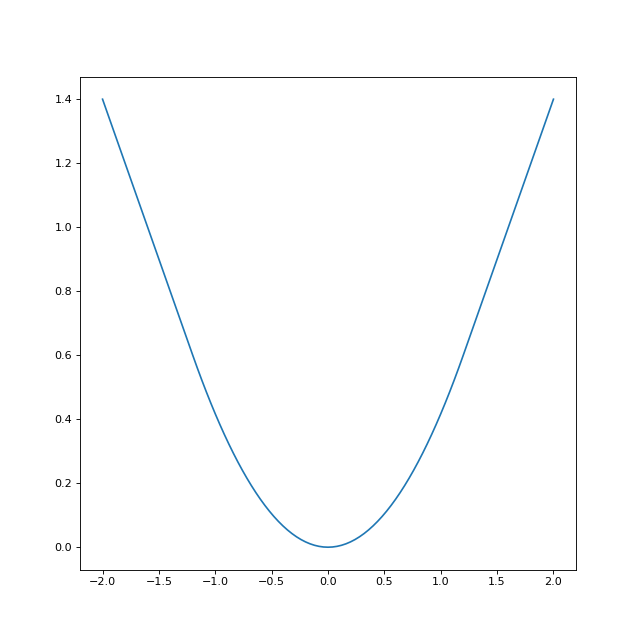

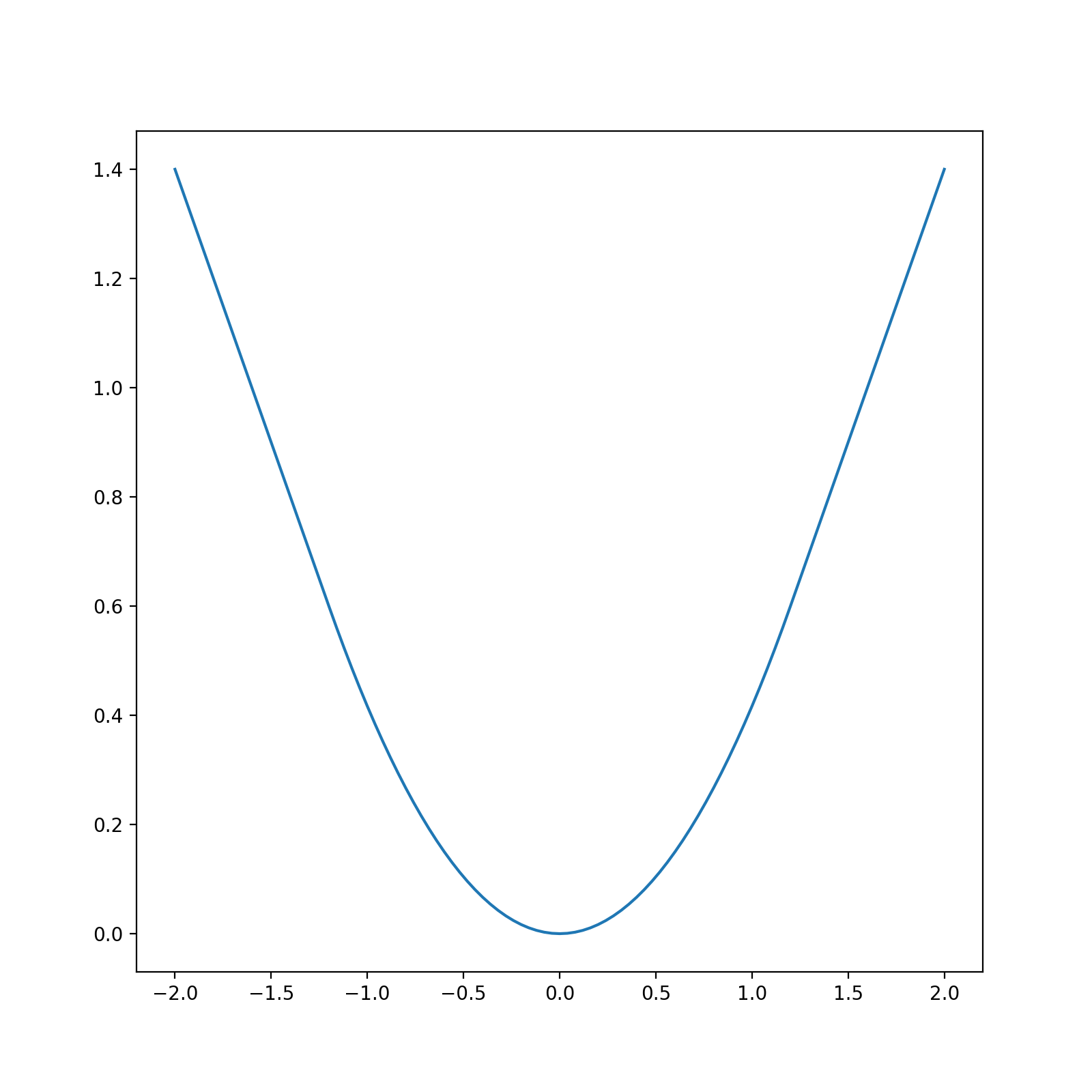

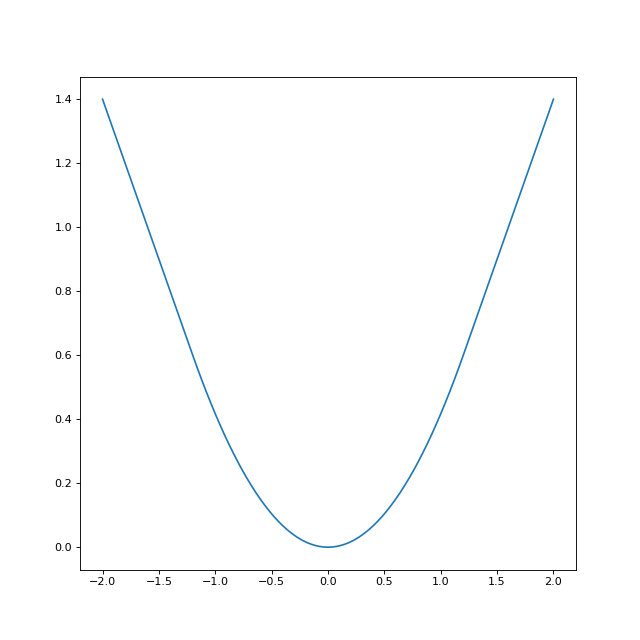

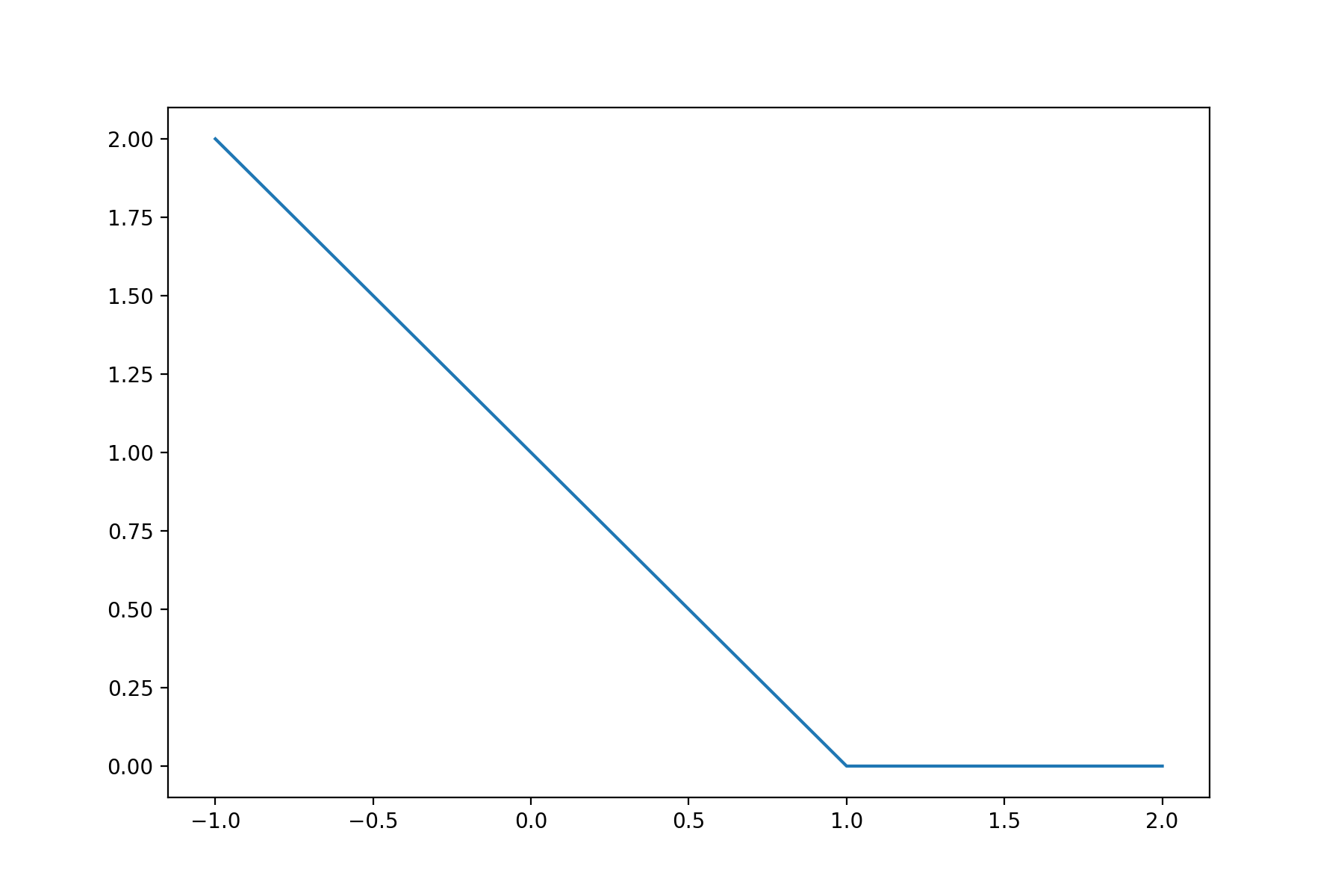

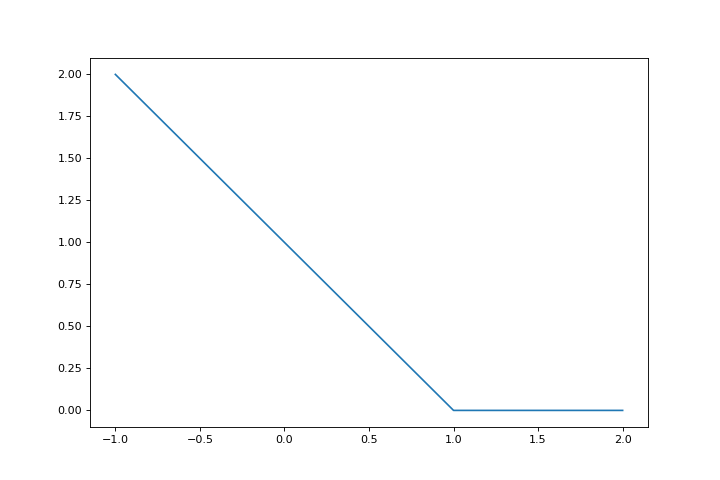

Let’s look at the Huber loss for a smoothing parameter of \(\delta=1.2\)

q = rr.identity_quadratic(1.2, 0., 0., 0.)

loss = rr.l1norm(1, lagrange=1).smoothed(q)

xval = np.linspace(-2,2,101)

yval = [loss.smooth_objective(x, 'func') for x in xval]

huber_fig = plt.figure(figsize=(8,8))

huber_ax = huber_fig.gca()

huber_ax.plot(xval, yval)

{kind=link}

{kind=link}

The Huber loss is built into regreg, but can also be obtained by

smoothing the l1norm atom. We will verify the two methods yield the

same solutions.

X = np.random.standard_normal((50, 10))

Y = np.random.standard_normal(50)

penalty = rr.l1norm(10,lagrange=5.)

loss_atom = rr.l1norm.affine(X, -Y, lagrange=1.).smoothed(rr.identity_quadratic(0.5,0,0,0))

loss = rr.glm.huber(X, Y, 0.5)

problem1 = rr.simple_problem(loss_atom, penalty)

print(problem1.solve(tol=1.e-12))

problem2 = rr.simple_problem(loss, penalty)

print(problem2.solve(tol=1.e-12))

Poisson regression tutorial¶

The Poisson regression problem minimizes the objective

which corresponds to the usual Poisson regression model

n = 100

p = 5

X = np.random.standard_normal((n,p))

Y = np.random.randint(0,100,n)

Now we can create the problem object, beginning with the loss function

loss = rr.glm.poisson(X, Y)

loss.solve()

rpy2.r.assign('Y', Y)

rpy2.r.assign('X', X)

np.array(rpy2.r('coef(glm(Y ~ X - 1, family=poisson()))'))

Logistic regression with a ridge penalty¶

In regreg, ridge penalties can be specified by the quadratic

attribute of a loss (or a penalty).

The regularized ridge logistic regression problem minimizes the objective

which corresponds to the usual logistic regression model

Let’s generate some sample data.

X = np.random.standard_normal((200, 10))

Y = np.random.randint(0,2,200)

Now we can create the problem object, beginning with the loss function

loss = rr.glm.logistic(X, Y)

penalty = rr.identity_quadratic(1., 0., 0., 0.)

loss.quadratic = penalty

loss

penalty.coef

1.0

loss.solve()

penalty.coef = 20.

loss.solve()

Multinomial regression¶

The multinomial regression problem minimizes the objective

which corresponds to a baseline category logit model for \(J\) nominal categories (e.g. Agresti, p.g. 272). For \(i \ne J\) the probabilities are measured relative to a baseline category \(J\)

from regreg.smooth.glm import multinomial_loglike

The only code needed to add multinomial regression to RegReg is a class with one method which computes the objective and its gradient.

Next, let’s generate some example data. The multinomial counts will be stored in a \(n \times J\) array

J = 5

n = 500

p = 10

X = np.random.standard_normal((n,p))

Y = np.random.randint(0,10,n*J).reshape((n,J))

Now we can create the problem object, beginning with the loss function. The coefficients will be stored in a \(p \times (J-1)\) array, and we need to let RegReg know that the coefficients will be a 2d array instead of a vector. We can do this by defining the input_shape in a linear_transform object that multiplies by X,

multX = rr.linear_transform(X, input_shape=(p,J-1))

loss = rr.multinomial_loglike.linear(multX, counts=Y)

loss.shape

Next, we can solve the problem

loss.solve()

When \(J=2\) this model should reduce to logistic regression. We can easily check that this is the case by first fitting the multinomial model

J = 2

Y = np.random.randint(0,10,n*J).reshape((n,J))

multX = rr.linear_transform(X, input_shape=(p,J-1))

loss = rr.multinomial_loglike.linear(multX, counts=Y)

solver = rr.FISTA(loss)

solver.fit(tol=1e-6)

multinomial_coefs = solver.composite.coefs.flatten()

Here is the equivalent logistic regresison model.

successes = Y[:,0]

trials = np.sum(Y, axis=1)

loss = rr.glm.logistic(X, successes, trials=trials)

solver = rr.FISTA(loss)

solver.fit(tol=1e-6)

logistic_coefs = solver.composite.coefs

Finally we can check that the two models gave the same coefficients

print(np.linalg.norm(multinomial_coefs - logistic_coefs) / np.linalg.norm(logistic_coefs))

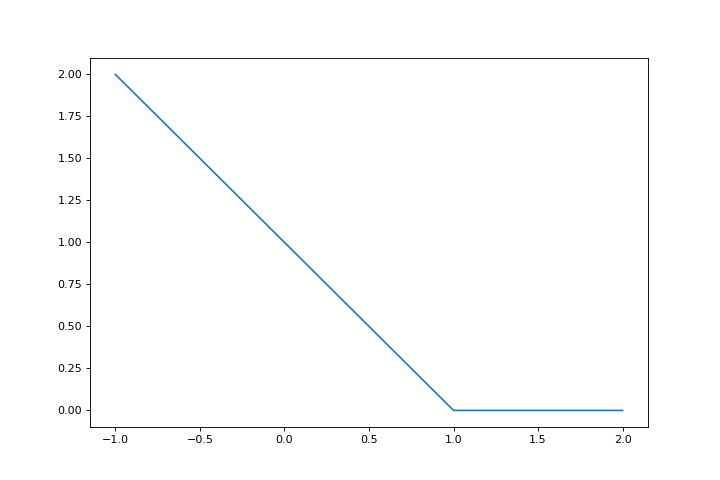

Hinge loss¶

The SVM can be parametrized various ways, one way to write it as a regression problem is to use the hinge loss:

hinge = lambda x: np.maximum(1-x, 0)

fig = plt.figure(figsize=(9,6))

ax = fig.gca()

r = np.linspace(-1,2,100)

ax.plot(r, hinge(r))

{kind=link}

{kind=link}

The SVM loss is then

where \(Y_i \in \{-1,1\}\) and \(X_i \in \mathbb{R}^p\) is one of the feature vectors.

In regreg, the hinge loss can be represented by composition of some of the basic atoms. Specifcally, let \(g:\mathbb{R}^n \rightarrow \mathbb{R}\) be the sum of positive part function

Then,

linear_part = np.array([[-1.]])

offset = np.array([1.])

hinge_rep = rr.positive_part.affine(linear_part, offset, lagrange=1.)

hinge_rep

Let’s plot the loss to be sure it agrees with our original hinge.

ax.plot(r, [hinge_rep.nonsmooth_objective(v) for v in r])

fig

Here is a vectorized version.

N = 1000

P = 200

Y = 2 * np.random.binomial(1, 0.5, size=(N,)) - 1.

X = np.random.standard_normal((N,P))

#X[Y==1] += np.array([30,-20] + (P-2)*[0])[np.newaxis,:]

X -= X.mean(0)[np.newaxis, :]

hinge_vec = rr.positive_part.affine(-Y[:, None] * X, np.ones_like(Y), lagrange=1.)

beta = np.ones(X.shape[1])

hinge_vec.nonsmooth_objective(beta), np.maximum(1 - Y * X.dot(beta), 0).sum()

Smoothed hinge¶

For optimization, the hinge loss is not differentiable so it is often smoothed first.

The smoothing is applicable to general functions of the form

where \(g_{\alpha}(z) = g(z-\alpha)\) and is determined by a small quadratic term

epsilon = 0.5

smoothing_quadratic = rr.identity_quadratic(epsilon, 0, 0, 0)

smoothing_quadratic

The quadratic terms are determined by four parameters with \((C_0, x_0, v_0, c_0)\).

Smoothing of the function by the quadratic \(q\) is performed by Moreau smoothing:

where

translation by \(-\alpha\).

The basic atoms in regreg know what their conjugate is. Our hinge

loss, hinge_rep, is the composition of an atom, and an affine

transform. This affine transform is split into two pieces, the linear

part, stored as linear_transform and its offset stored as

atom.offset. It is stored with atom as atom needs knowledge

of this when computing proximal maps.

hinge_rep.atom

hinge_rep.atom.offset

hinge_rep.linear_transform.linear_operator

As we said before, hinge_rep.atom knows what its conjugate is

hinge_conj = hinge_rep.atom.conjugate

hinge_conj

The notation \(I^{\infty}\) denotes a constraint. The expression can therefore be parsed as a linear function \(\eta^T\beta\) plus the function

The term \(\eta\) is derived from hinge_rep.atom.offset and is

stored in hinge_conj.quadratic.

hinge_conj.quadratic.linear_term

Now, let’s look at the smoothed hinge loss.

smoothed_hinge_loss = hinge_rep.smoothed(smoothing_quadratic)

smoothed_hinge_loss

It is now a smooth function and its objective value and gradient can be

computed with smooth_objective.

ax.plot(r, [smoothed_hinge_loss.smooth_objective(v, 'func') for v in r])

fig

less_smooth = hinge_rep.smoothed(rr.identity_quadratic(5.e-2, 0, 0, 0))

ax.plot(r, [less_smooth.smooth_objective(v, 'func') for v in r])

fig

Fitting the SVM¶

We can now minimize this objective.

smoothed_vec = hinge_vec.smoothed(rr.identity_quadratic(0.2, 0, 0, 0))

soln = smoothed_vec.solve(tol=1.e-12, min_its=100)

Sparse SVM¶

We might want to fit a sparse version, adding a sparsifying penalty like the LASSO. This yields the problem

penalty = rr.l1norm(smoothed_vec.shape, lagrange=20)

problem = rr.simple_problem(smoothed_vec, penalty)

problem

sparse_soln = problem.solve(tol=1.e-12)

sparse_soln

What value of \(\lambda\) should we use? For the \(\ell_1\) penalty in Lagrange form, the smallest \(\lambda\) such that the solution is zero can be found by taking the dual norm, the \(\ell_{\infty}\) norm, of the gradient of the smooth part at 0.

linf_norm = penalty.conjugate

linf_norm

Just computing the conjugate will yield an \(\ell_{\infty}\) constraint, but this object can still be used to compute the desired value of \(\lambda\).

score_at_zero = smoothed_vec.smooth_objective(np.zeros(smoothed_vec.shape), 'grad')

lam_max = linf_norm.seminorm(score_at_zero, lagrange=1.)

lam_max

penalty.lagrange = lam_max * 1.001

problem.solve(tol=1.e-12, min_its=200)

penalty.lagrange = lam_max * 0.99

problem.solve(tol=1.e-12, min_its=200)

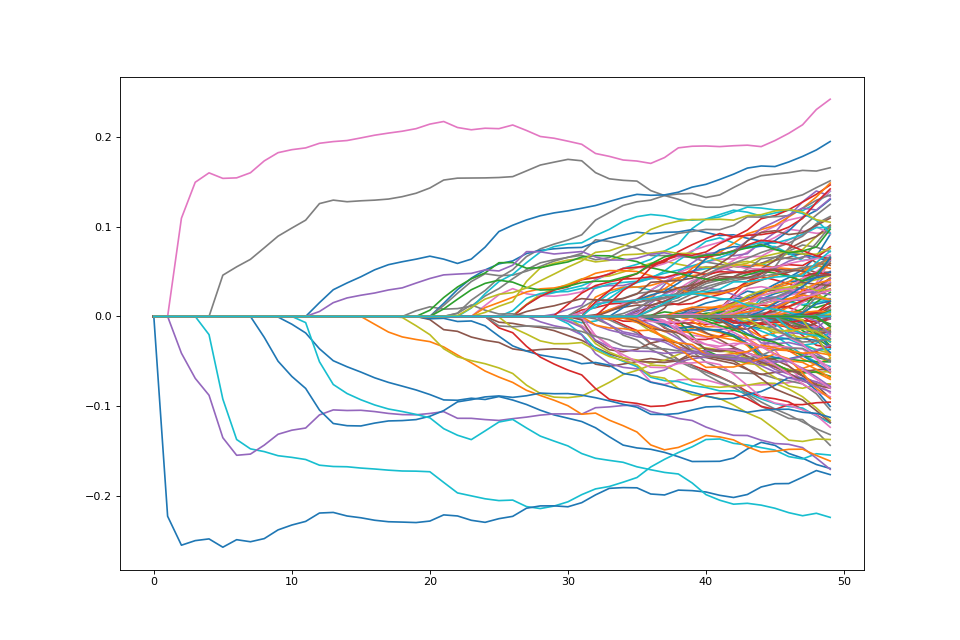

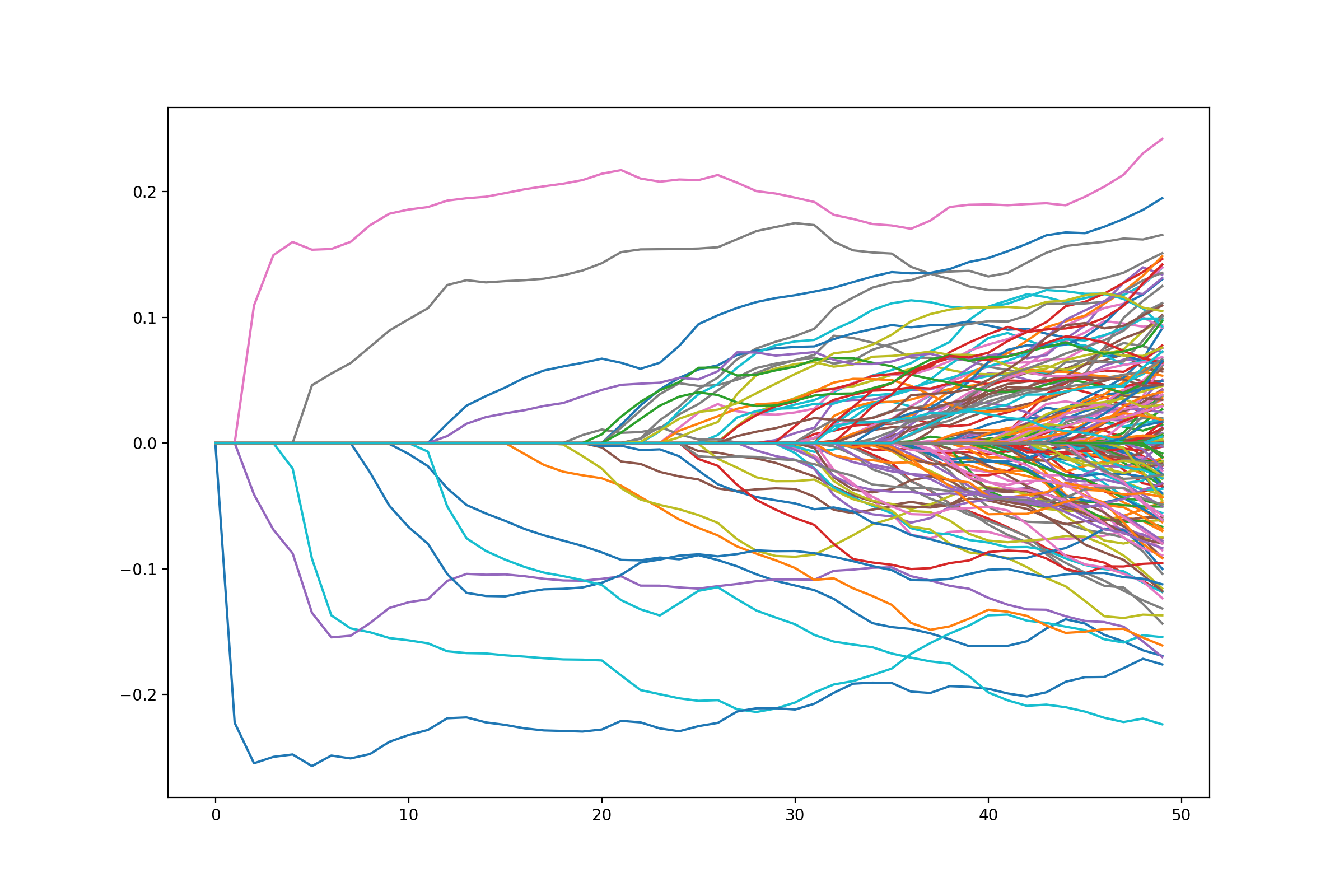

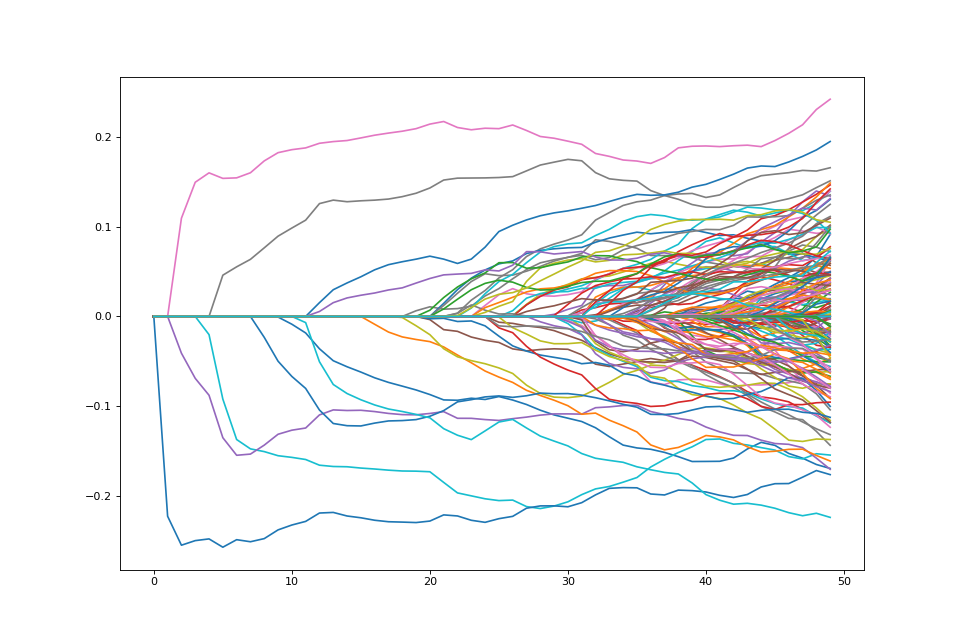

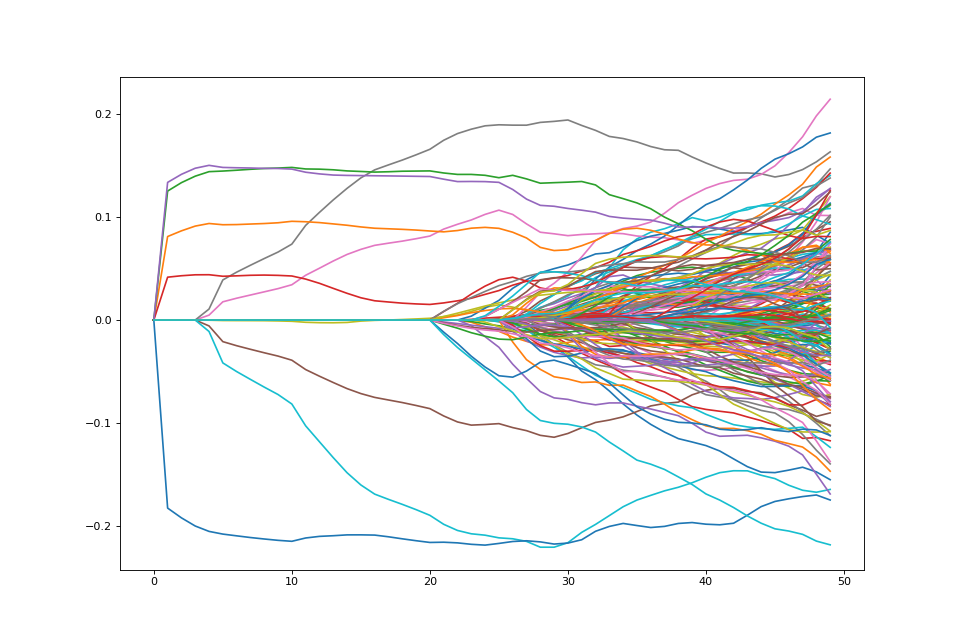

Path of solutions¶

If we want a path of solutions, we can simply take multiples of

lam_max. This is similar to the strategy that packages like

glmnet use

path = []

lam_vals = (np.linspace(0.05, 1.01, 50) * lam_max)[::-1]

for lam_val in lam_vals:

penalty.lagrange = lam_val

path.append(problem.solve(min_its=200).copy())

fig = plt.figure(figsize=(12,8))

ax = fig.gca()

path = np.array(path)

ax.plot(path);

{kind=link}

{kind=link}

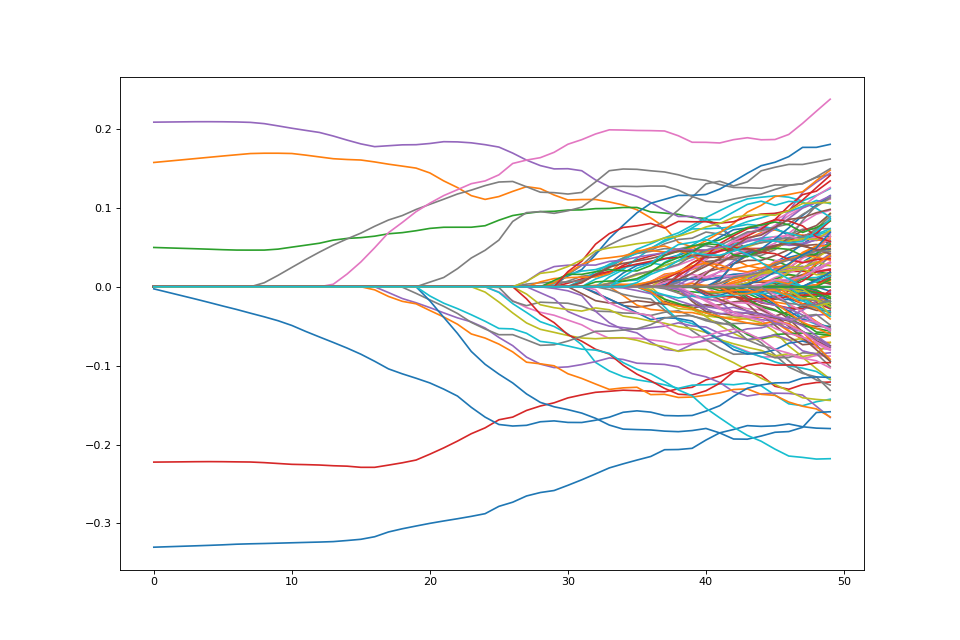

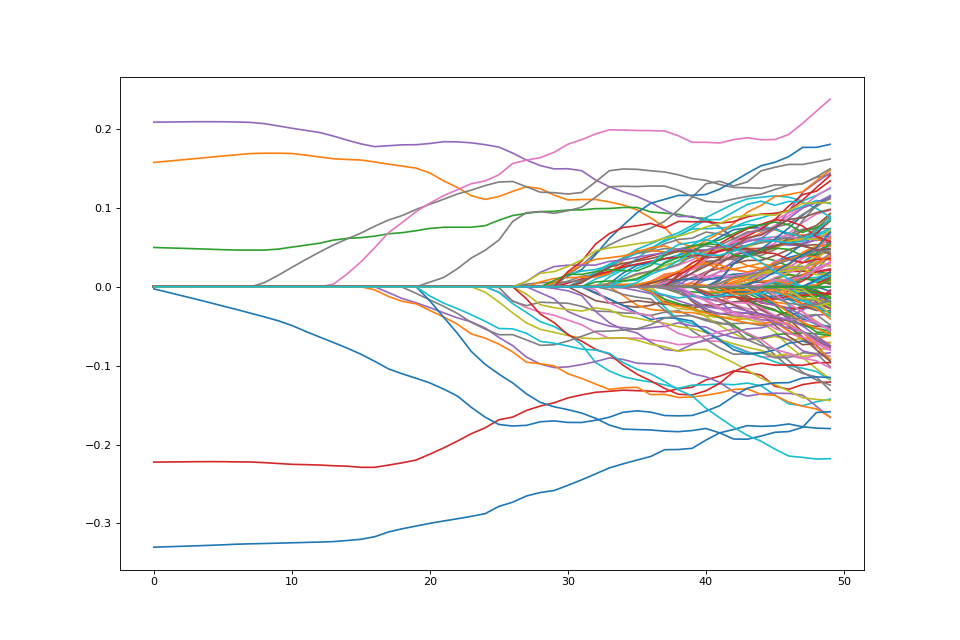

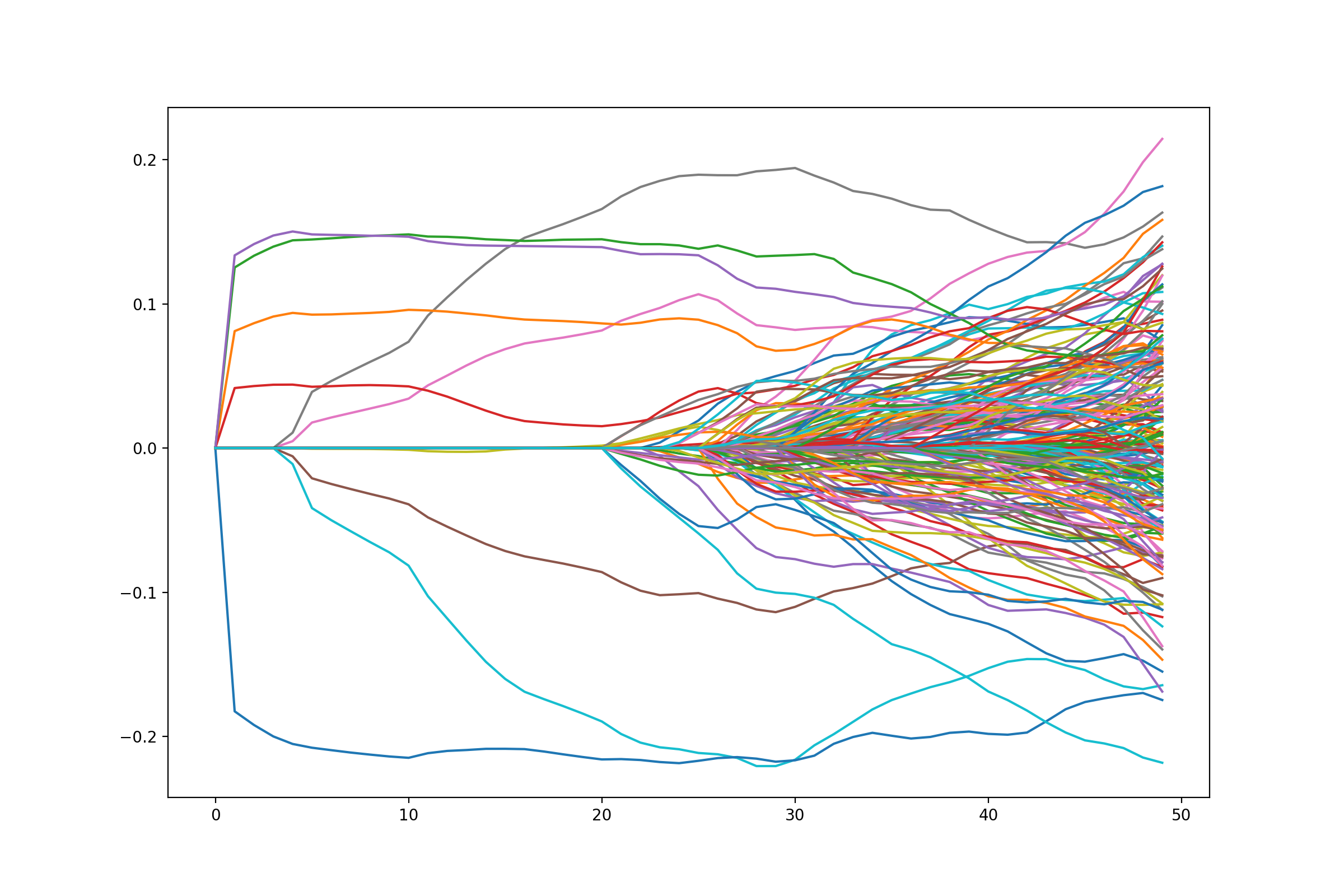

Changing the penalty¶

We may not want to penalize features the same. We may want some features to be unpenalized. This can be achieved by introducing possibly non-zero feature weights to the \(\ell_1\) norm

weights = np.random.sample(P) + 1.

weights[:5] = 0.

weighted_penalty = rr.weighted_l1norm(weights, lagrange=1.)

weighted_penalty

weighted_dual = weighted_penalty.conjugate

weighted_dual

lam_max_weight = weighted_dual.seminorm(score_at_zero, lagrange=1.)

lam_max_weight

weighted_problem = rr.simple_problem(smoothed_vec, weighted_penalty)

path = []

lam_vals = (np.linspace(0.05, 1.01, 50) * lam_max_weight)[::-1]

for lam_val in lam_vals:

weighted_penalty.lagrange = lam_val

path.append(weighted_problem.solve(min_its=200).copy())

fig = plt.figure(figsize=(12,8))

ax = fig.gca()

path = np.array(path)

ax.plot(path);

{kind=link}

{kind=link}

Note that there are 5 coefficients that are not penalized hence they are nonzero the entire path.

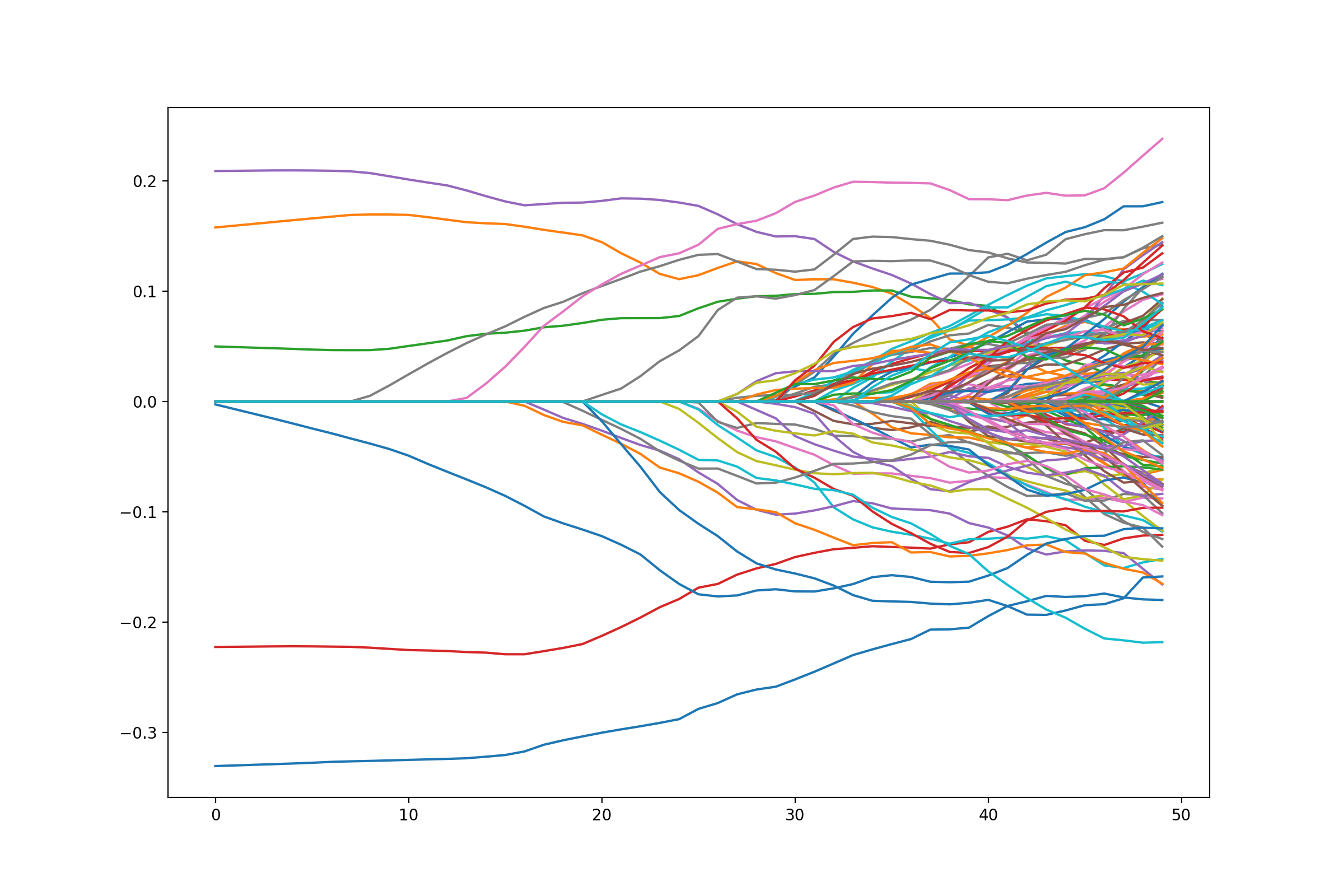

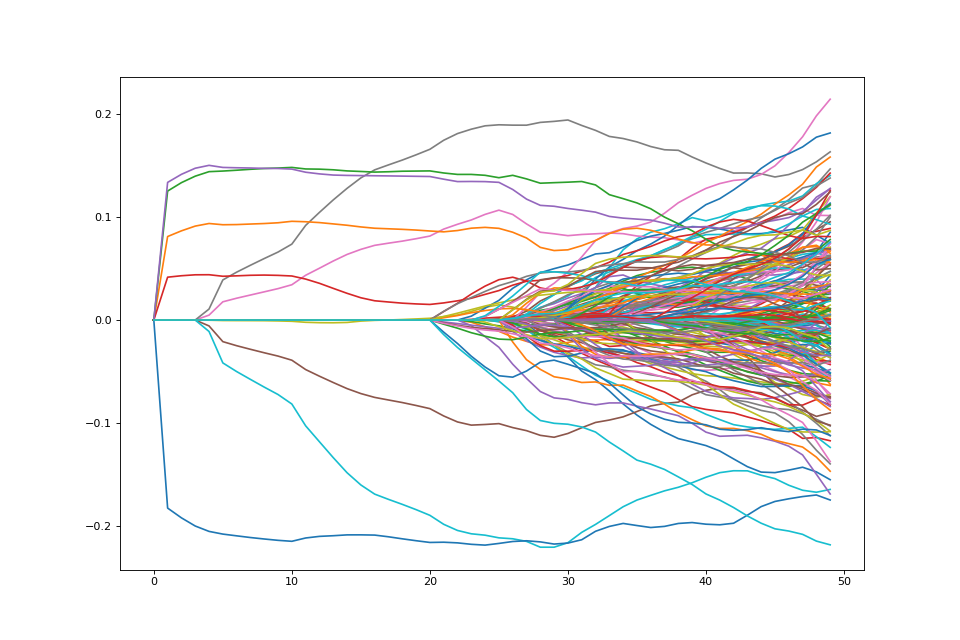

Variables may come in groups. A common penalty for this setting is the group LASSO. Let

be a partition of the set of features and \(w_g\) a weight for each group. The group LASSO penalty is

groups = []

for i in range(int(P/5)):

groups.extend([i]*5)

weights = dict([g, np.random.sample()+1] for g in np.unique(groups))

group_penalty = rr.group_lasso(groups, weights=weights, lagrange=1.)

group_dual = group_penalty.conjugate

lam_max_group = group_dual.seminorm(score_at_zero, lagrange=1.)

group_problem = rr.simple_problem(smoothed_vec, group_penalty)

path = []

lam_vals = (np.linspace(0.05, 1.01, 50) * lam_max_group)[::-1]

for lam_val in lam_vals:

group_penalty.lagrange = lam_val

path.append(group_problem.solve(min_its=200).copy())

fig = plt.figure(figsize=(12,8))

ax = fig.gca()

path = np.array(path)

ax.plot(path);

{kind=link}

{kind=link}

As expected, variables enter in groups here.

Bound form¶

The common norm atoms also have a bound form. That is, we can just as easily solve the problem

bound_l1 = rr.l1norm(P, bound=2.)

bound_l1

bound_problem = rr.simple_problem(smoothed_vec, bound_l1)

bound_problem

bound_soln = bound_problem.solve()

np.fabs(bound_soln).sum()

Support vector machine¶

This tutorial illustrates one version of the support vector machine, a linear example. The minimization problem for the support vector machine, following ESL is

We use the \(C\) parameterization in (12.25) of ESL

This is an example of the positive part atom combined with a smooth quadratic penalty. Above, the \(x_i\) are rows of a matrix of features and the \(y_i\) are labels coded as \(\pm 1\).

Let’s generate some data appropriate for this problem.

import numpy as np

>>>

np.random.seed(400) # for reproducibility

N = 500

P = 2

>>>

Y = 2 * np.random.binomial(1, 0.5, size=(N,)) - 1.

X = np.random.standard_normal((N,P))

X[Y==1] += np.array([3,-2])[np.newaxis,:]

X -= X.mean(0)[np.newaxis,:]

from sklearn.svm import SVC

clf = SVC(kernel='linear')

X = np.array([[-1, -1], [-2, -1], [1, 1], [2, 1]])

y = np.array([1, 1, 2, 2])

clf.fit(X, y)

print(clf.coef_, clf.dual_coef_, clf.support_)

The hinge loss is not smooth, but it can be written as the composition

of an atom (positive_part) with an affine transform determined

by the data.

Such objective functions can be smoothed. NESTA and TFOCS describe schemes in which smoothing of these atoms can be used to produce optimization problems with smooth objectives which can have additional structure imposed through optimization.

Let us try smoothing the objective and using NESTA by smoothing the hinge loss. Of course, one can also solve the usual SVC dual problem by smoothing.

def nesta_svm(X, y_pm, C=1.):

n, p = X.shape

X_1 = np.hstack([X, np.ones((X.shape[0], 1))])

hinge_loss = rr.positive_part.affine(-y_pm[:,None] * X_1, + np.ones(n),

lagrange=C)

selector = np.identity(p+1)[:p]

smooth_ = rr.quadratic_loss.linear(selector)

soln = rr.nesta(smooth_, None, hinge_loss)

return soln[0][:-1], soln[1]

nesta_svm(X, 2 * (y - 1.5))

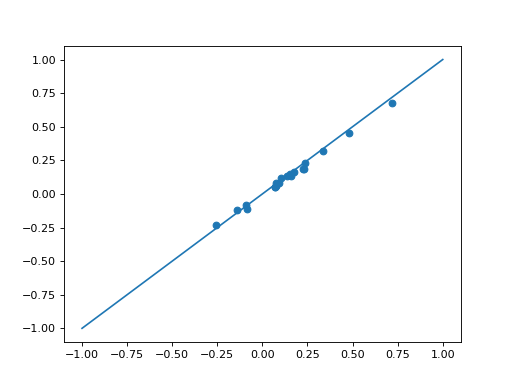

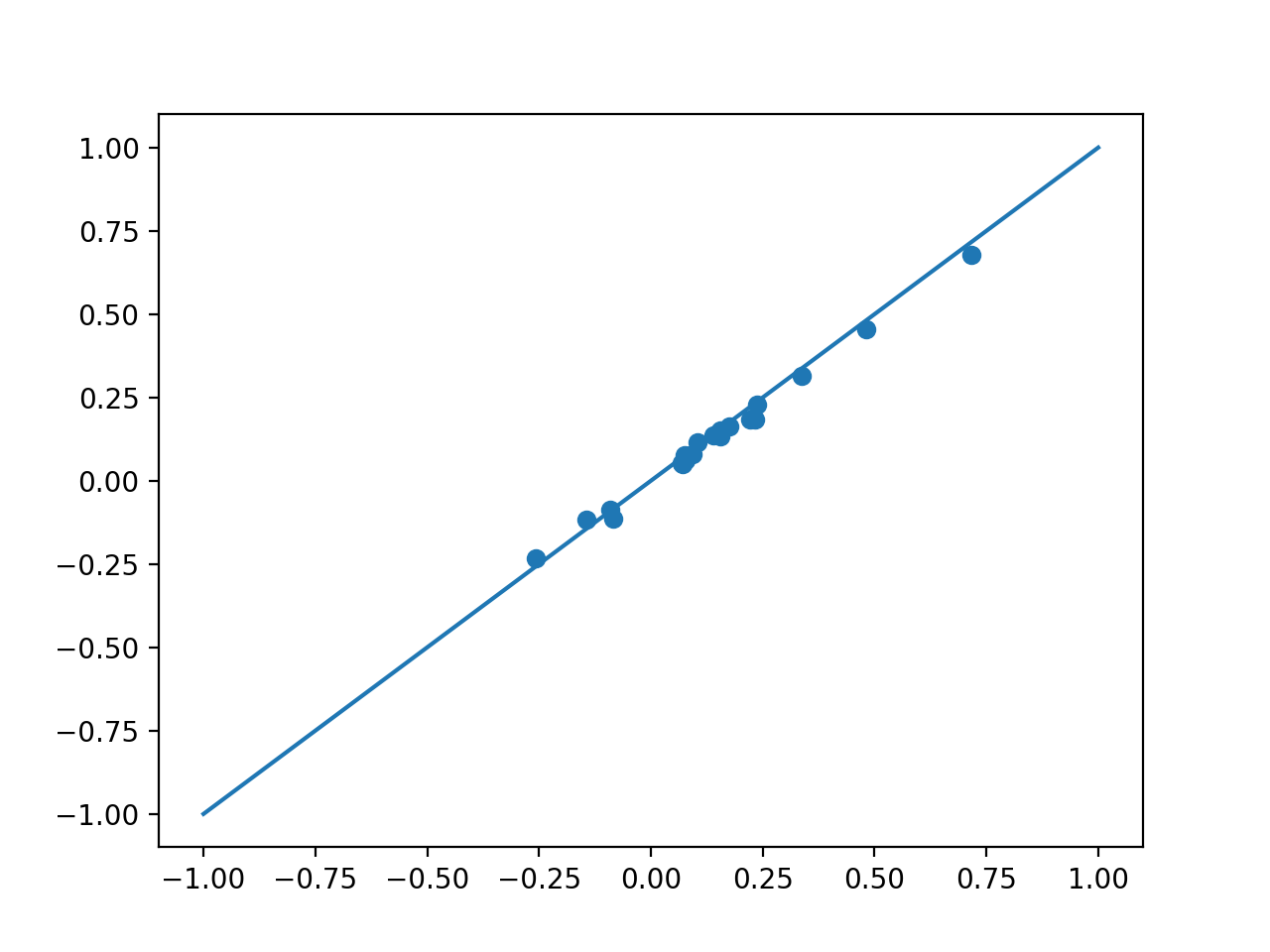

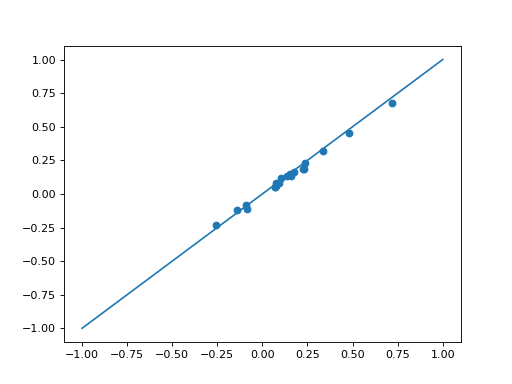

Let’s try a little larger data set.

X_l = np.random.standard_normal((100, 20))

Y_l = 2 * np.random.binomial(1, 0.5, (100,)) - 1

C = 4.

clf = SVC(kernel='linear', C=C)

clf.fit(X_l, Y_l)

clf.coef_

solnR_ = nesta_svm(X_l, Y_l, C=C)[0]

plt.scatter(clf.coef_, solnR_)

plt.plot([-1,1], [-1,1])

{kind=link}

{kind=link}

Using regreg, we can easily add penalty or constraint to the SVM

objective.

def nesta_svm_pen(X, y_pm, atom, C=1.):

n, p = X.shape

X_1 = np.hstack([X, np.ones((X.shape[0], 1))])

hinge_loss = rr.positive_part.affine(-y_pm[:,None] * X_1, + np.ones(n),

lagrange=C)

selector = np.identity(p+1)[:p]

smooth_ = rr.quadratic_loss.linear(selector)

atom_sep = rr.separable((p+1,), [atom], [slice(0,p)])

soln = rr.nesta(smooth_, atom_sep, hinge_loss)

return soln[0][:-1]

bound = rr.l1norm(20, bound=0.8)

nesta_svm_pen(X_l, Y_l, bound)

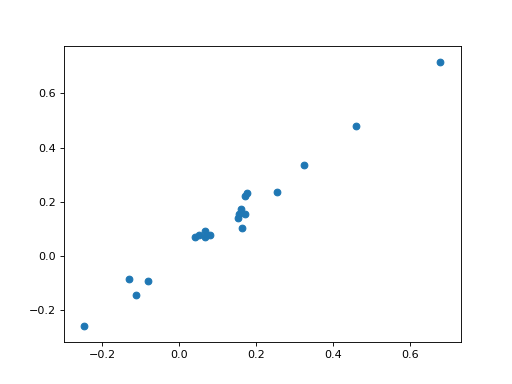

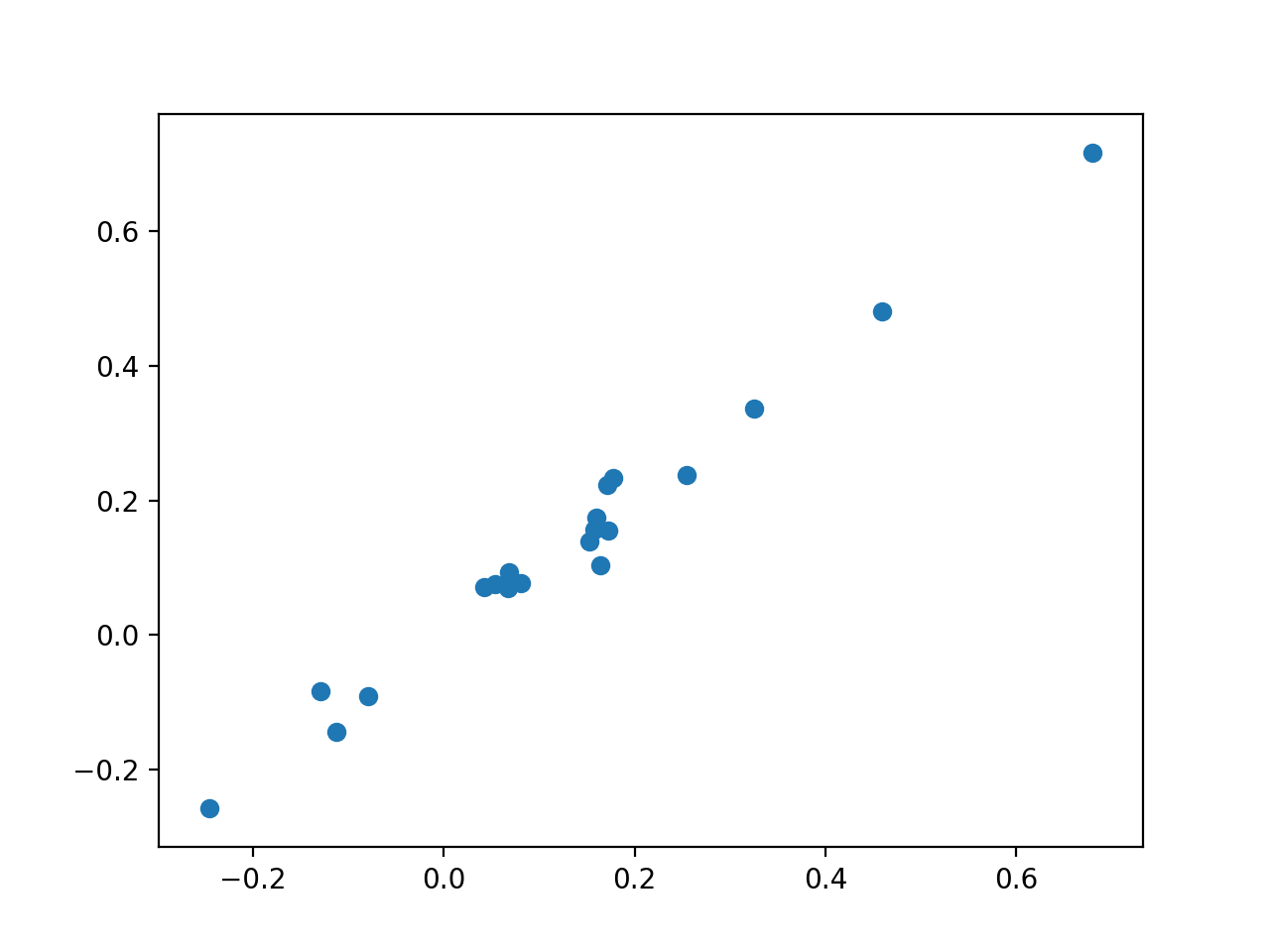

Sparse Huberized SVM¶

Instead of using NESTA we can just smooth the SVM with a fixed smoothing parameter and solve the problem directly.

from regreg.smooth.losses import huberized_svm

X_l_inter = np.hstack([X_l, np.ones((X_l.shape[0],1))])

huber_svm = huberized_svm(X_l_inter, Y_l, smoothing_parameter=0.001, coef=C)

coef_h = huber_svm.solve(min_its=100)[:-1]

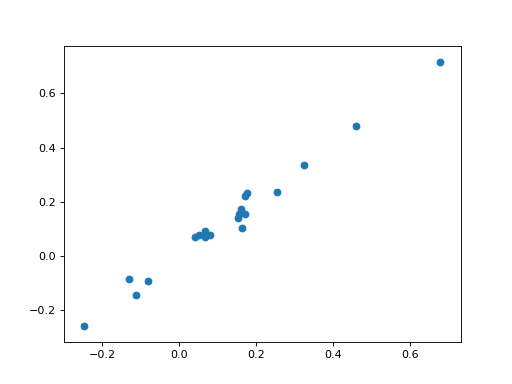

plt.scatter(coef_h, clf.coef_)

{kind=link}

{kind=link}

Adding penalties or constraints is again straightforward.

penalty = rr.l1norm(X_l.shape[1], lagrange=8.)

penalty_sep = rr.separable((X_l.shape[1]+1,), [penalty], [slice(0,X_l.shape[1])])

huberized_problem = rr.simple_problem(huber_svm, penalty_sep)

huberized_problem.solve()

numpy2ri.deactivate()